EarnIn: Why Wait for Payday?

Overview

The EarnIn app serves as a prominent platform in the Earned Wage Access (EWA) market. It comes with core utility: enabling hourly and salaried employees to access their earned wages prior to the termination of the standard bi-weekly or monthly payroll cycle.

Historically, workers experiencing mid-cycle cash shortfalls were forced to rely on high-interest payday loans, expensive credit lines, or bank overdraft fees. EarnIn addresses this vulnerability by treating the user's documented, accumulated labor hours as a secure asset.

The primary mechanism of the platform relies on establishing a secure connection to the user's primary checking account and payroll ledger. Through Plaid API integrations, the application monitors transaction histories and direct deposit patterns to verify income consistency.

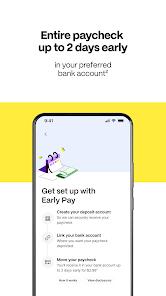

To calculate a user's real-time earnings, the app processes electronic timesheet uploads or uses location-based GPS tracking to confirm the user's physical presence at their workplace.

EarnIn operates under a voluntary payment model. Instead of charging interest or mandatory fees, the app allows users to pay what they deem fair through optional "tips," which help support the platform's infrastructure and keep basic services free.

Additionally, the app features "Balance Shield," an automated tool designed to help users avoid overdraft fees. By continuously monitoring the connected bank account, Balance Shield can send low-balance alerts and automatically trigger a cash advance of up to $100 to keep the account balance positive.

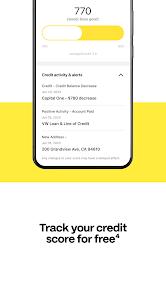

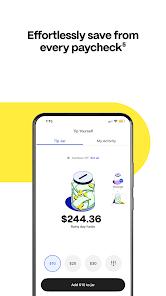

The app also provides automated micro-savings through "Tip Yourself" and free credit score tracking via Experian's VantageScore 3.0 model, helping users build long-term financial stability.

Pros & Cons

Mitigation of Predatory Debt: The application provides a non-interest, zero-fee alternative to high-interest payday loans, helping users avoid predatory debt cycles.

Flexible Funding Speeds: Users can choose between completely free standard transfers or pay a low $2.99 fee for instant "Lightning Speed" deposits.

Proactive Overdraft Prevention: The Balance Shield feature monitors linked accounts and automatically sweeps in funds to help users avoid bank overdraft charges.

Credit Score Tracking: Integrates free VantageScore 3.0 monitoring directly into the dashboard, helping users stay informed about their credit health.

Inclusive Eligibility Criteria: Because the underwriting process relies on banking ledger history rather than credit scores, the platform remains accessible to individuals with poor or limited credit history.

- ✕

Plaid Connection Instability: Frequent API connection drops can require repeated bank re-authentication, which can delay access to funds during emergencies.

- ✕

Intrusive Geolocation Demands: The app's dependency on continuous background GPS geofencing to verify work hours can accelerate battery drain and raise privacy concerns.

- ✕

Rigid Income Requirements: The platform excludes gig-economy workers, cash-paid employees, and individuals with irregular pay cycles by requiring a consistent direct deposit history.

- ✕

Daily Liquidity Limitations: The daily withdrawal limit of $150 can prevent users from covering larger, sudden expenses in a single day.

Download

FAQs

Is EarnIn legally classified as a payday lender?

No, EarnIn is not a payday lender or a bank. Its services are structured as non-recourse advances on wages the user has already earned, meaning the transactions do not charge interest, do not require credit checks, and do not carry a legal obligation of debt.

How does the application verify working hours for remote or salaried employees?

For salaried or remote employees who cannot use GPS-based geofencing, EarnIn verifies hours by linking to electronic timesheet portals, uploading PDF paystubs, or tracking company-specific email domains.

Does using the EarnIn application impact the user's credit score?

No, using EarnIn has no direct impact on credit ratings. The developer does not perform hard or soft credit checks during registration, nor does the platform report payment histories or defaults to the credit bureaus.

What happens if the connected bank account has insufficient funds on payday?

EarnIn is designed to automatically recover advanced funds via an ACH debit sweep on the user's scheduled payday. If the sweep fails due to insufficient funds, EarnIn will suspend the account and block future advances until the balance is repaid, though it does not charge late fees.

How does the Balance Shield feature operate?

Balance Shield is an automated tool that monitors the linked bank ledger. If the account balance falls below a user-defined threshold, the feature automatically sweeps up to $100 of earned wages into the account to prevent overdrafts.

Hot Reviews

The application allowed for an immediate $150 transfer to cover unexpected car repairs, helping avoid high-interest options or credit card debt when cash was tight mid-month.

A recent software update has caused the app to repeatedly disconnect from linked bank accounts, forcing users to log in through Plaid multiple times a day just to check their limits.

While the cash advance feature works well, the app's requirement for continuous GPS tracking to verify work hours is overly intrusive and drains phone battery life quickly.

The platform is a great option for individuals with lower credit scores since eligibility is based entirely on consistent direct deposit history rather than traditional credit checks.